|

|

|

|

|

| |

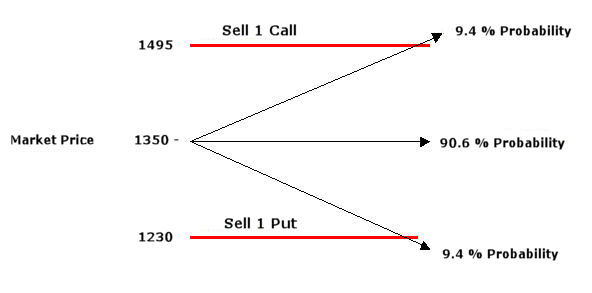

| The primary Optioneer methodology is based upon an option trading strategy known as a short strangle. A short strangle involves selling an out-of-the-money call option and an out-of-the-money put option on the same underlying asset with the same expiration date. To manage risk, the options are written far out-of-the-money so that the chances of the market price reaching the sold call or put boundary, by expiration date, are greatly reduced.*

Optioneer uses a proprietary algorithm to determine what strike prices to sell and when to sell them. These trades are presented to each client on a daily basis. The typical Optioneer trade is constructed based upon a proprietary probability calculation of 9.4%. This means that on the day the trade is set, there is a 9.4% probability of the market price closing above the sold call or below the sold put strike price by expiration date. That means there is a great likelihood that the market price will not breach the sold boundaries during the lifecycle of the trade. These probability calculations are a key part of managing the risk within the trade.**

See the example listed below. (S&P; 500 example) |

| |

|

| * There is a substantial risk of loss associated with trading futures and options on futures.

** No representation is being made that users of the methodology will or are likely to realize profits or avoid losses on a certain percentage of trades. |

| |

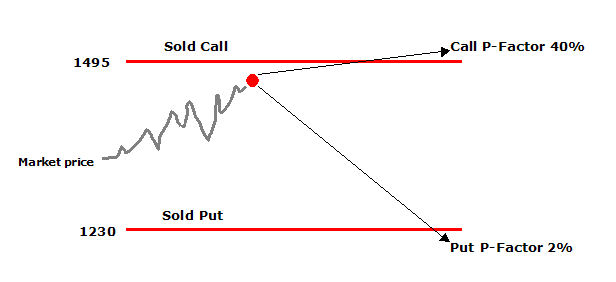

| Once an Optioneer trade is entered the seller of the option is obligated to pay the buyer of the option a certain amount of money for every point that the underlying asset trades beyond the sold call or sold put boundaries.

For this reason, option sellers never want the options market price to break through their sold options. Optioneer calculates and reports the Probability Factors for the sold puts and calls on a daily basis. Probability Factors will fluctuate each day depending on the underlying asset’s daily movement. As long as the trade’s Probability Factors stay below 40% the trade may be maintained. However, if the Probability Factors ever reach a reading of 40% or more, the Optioneer strategy provides a guideline for exiting the trade before the market breaks through one of the sold boundaries.

See example listed below. (S&P; 500 example) |

|

| In this particular example the market price has moved much closer to the sold call position throughout the duration of the trade. On this day, a 40% Probability Factor reading has been reached on the call side of the trade. This means that according to our proprietary Probability Factor, the market price has a 40% probability of finishing above our sold call position by expiration date. Additionally, it means that the market price has a 60% probability of finishing below the sold call at expiration. At this point, the reward to risk balance is no longer in our favor, and so, according to our rules, we recommend exiting the trade.

By simply monitoring the probability factors of both the sold call and put at the end of each trading day, a trader can identify which trades should be maintained and which trades to should consider exiting early.

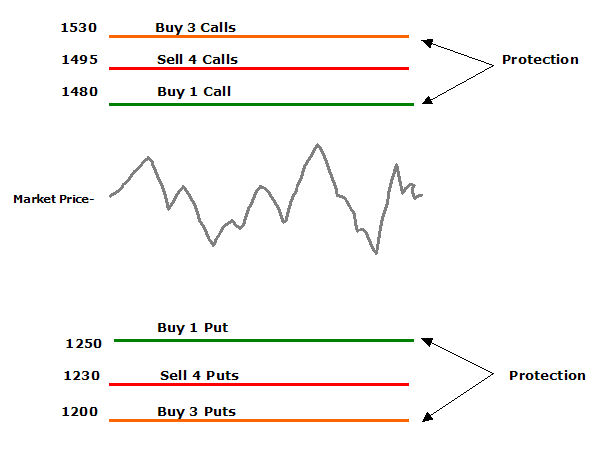

Although the Probability Factor report comes out at the end of each day, there are extreme circumstances where the P-Factor would not be useful; for example, September 11th or the market crash in 1987. When something dramatic like this happens the market typically overreacts and large swings can take place. At these times the probability factors would be useless because the market moved so quickly that there was not time to react. In response to this, Optioneer has developed risk reduction strategies to protect against unlimited risk. For each Optioneer trade, clients can hedge their sold option positions by purchasing options at precisely calculated levels. For every option that is sold the strategy suggests purchasing a corresponding risk-limiting option. By purchasing these protective options above and below each sold call and put, a trader can limit his/her market exposure in the event of a severe or sudden move in the market. Below is an example of what a trade might look like.

(S&P; 500 Hybrid Example) |

|

Due to an individual’s varying investment objectives, Optioneer has developed three protective strategies with varying risk profiles. They are as follows:

- Hybrid

The Hybrid is the preferred and most conservative trading model that Optioneer offers. It is suited for a volatile market.

- Iron Condor

The Iron Condor is considered to be the most aggressive trading model that Optioneer offers. It is suited for a stable market.

- Hybridor

The Hybridor is a combination of the Hybrid and Iron Condor trading models. It is therefore not considered to be aggressive or conservative but somewhere in between. It is suited for a stable or bearish market.

|

| By combining the Optioneer Probability Technology with specific risk management strategies geared to each trader’s specific needs, the Optioneer client can manage complex option trades with confidence. |

|

|

|

|

|

|

|